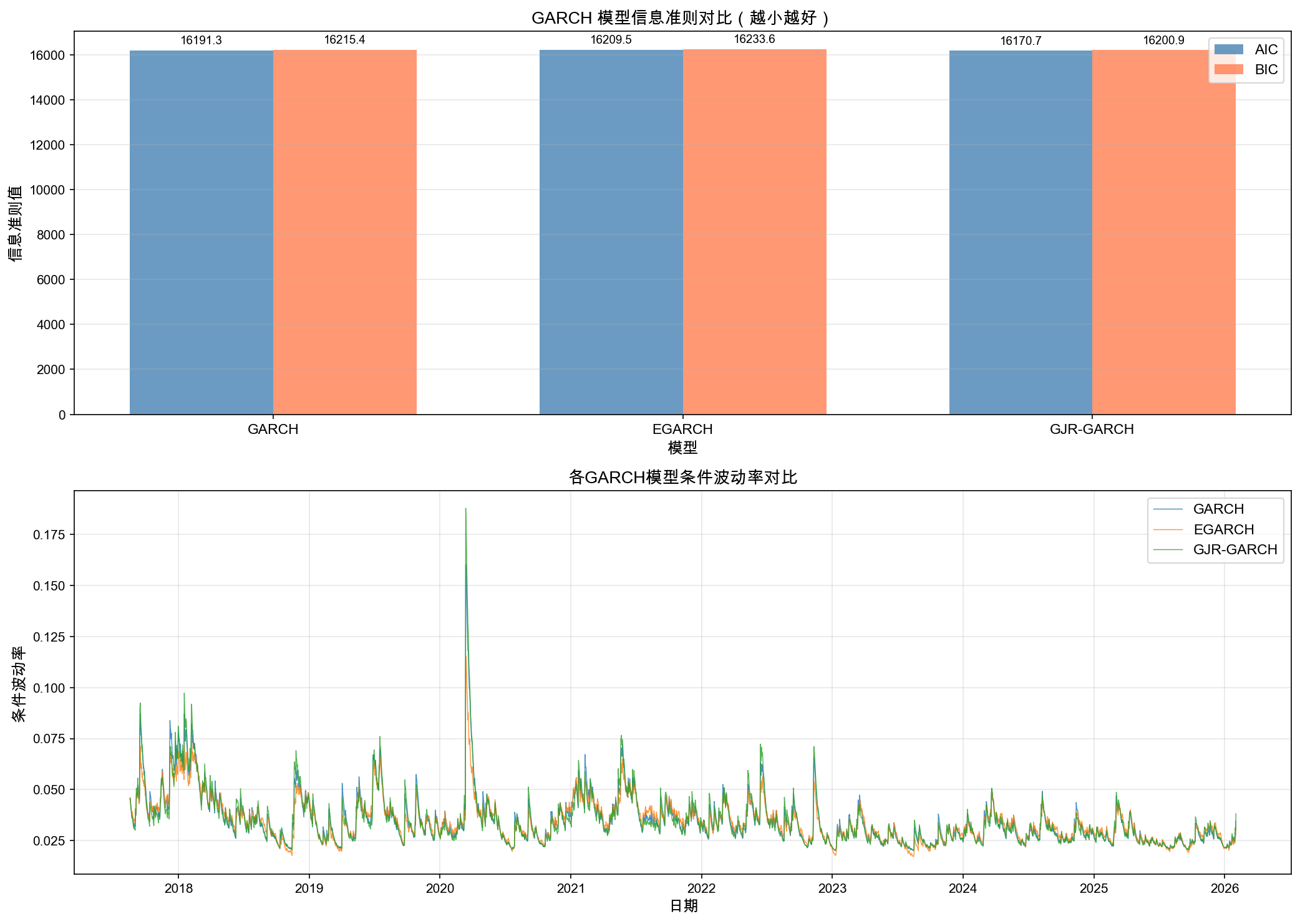

Complete statistical analysis pipeline covering: - FFT spectral analysis, wavelet CWT, ACF/PACF autocorrelation - Returns distribution (fat tails, kurtosis=15.65), GARCH volatility modeling - Hurst exponent (H=0.593), fractal dimension, power law corridor - Volume-price causality (Granger), calendar effects, halving cycle analysis - Technical indicator validation (0/21 pass FDR), candlestick pattern testing - Market state clustering (K-Means/GMM), Markov chain transitions - Time series forecasting (ARIMA/Prophet/LSTM benchmarks) - Anomaly detection ensemble (IF+LOF+COPOD, AUC=0.9935) Key finding: volatility is predictable (GARCH persistence=0.973), but price direction is statistically indistinguishable from random walk. Includes REPORT.md with 16-section analysis report and future projections, 70+ charts in output/, and all source modules in src/. Co-Authored-By: Claude Opus 4.5 <noreply@anthropic.com>

234 KiB

2084x1482px

234 KiB

2084x1482px

{kind=link}

{kind=link}